Understanding venture dilution in biotech

If you read any one of dozens of books on raising venture capital dollars (I recommend Venture Deals in particular), you will likely hear that a typical raise will dilute the current shareholders between 20-35%.

In biotech it is widely accepted that dilution can be much more, in no small part because the early capital raises are often much higher than in tech when the perceived risk is still high (ie: $10-40M for a Series A easily, with no clinical data).

New biotech founders are at a serious information disadvantage, since there just isn't as much available information for them in this space as there is for their internet counterparts.

Until now...

Let me just say, as a founder dilution should not be your primary concern. Biotech can have somewhat binary exits - either 0 dollars or large sums, with relatively few "salvage sales". The right partner or VC can drive you through a milestone that increases your value dramatically and results in an overall net gain on your stock holdings regardless of apparently large dilution.

If you haven't seen it already, I highly recommend Paul Graham's essay on The Equity Equation, which does a deep dive on just this concept.

Still, it is important to understand what is normal. This can prevent founders from appearing naïve by asking for too much or too little value for their equity, and can prevent predatory venture deals. Promising technologies have been ruined by cap tables polluted with bad investors who took too much for too little value, and worse may have control stakes in a company which prevent a recapitalization.

Understanding typical dilution in biotech

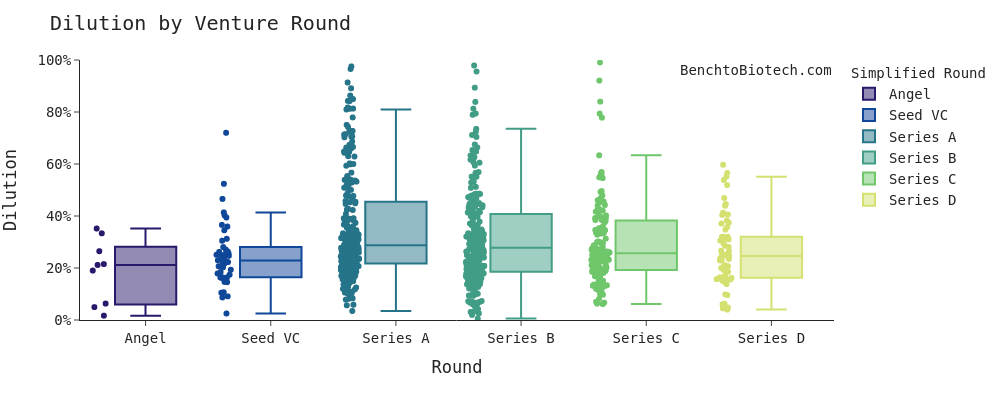

Below is data from 744 unique rounds from 407 cancer therapeutics companies with both capital raise and valuation information available.

An important caveat here - these are private companies, so this data could be incomplete or straight up wrong in many cases. Companies are under no obligation to share information about debt, warrants, stock pools, or other issuances and usually wouldn't. Also, dilution near 100% is more likely to be a "venture studio" deal, where the venture firm takes a direct role in company formation and incentivizes the management team from issuances that are not reflected directly in the raise.

Use these as "guidelines", not rules or advice

Also, if all of the above terms and the references to Series below seem like another language to you, I can't recommend the Venture Deals book enough. I don't make any money off of that, I just really like the stonk.

Ok, that's it for disclaimers and caveats, let's get into it.

Right away, we see something surprising. Although dilution ranges from minimal to nearly 100% in many cases, the typical dilution for a Series A round falls between 22-45% (median 29%). For Series B, you see 19-41% (median 28%). Although it's at the higher end, this isn't really that far off of what you would expect to see in a tech deal.

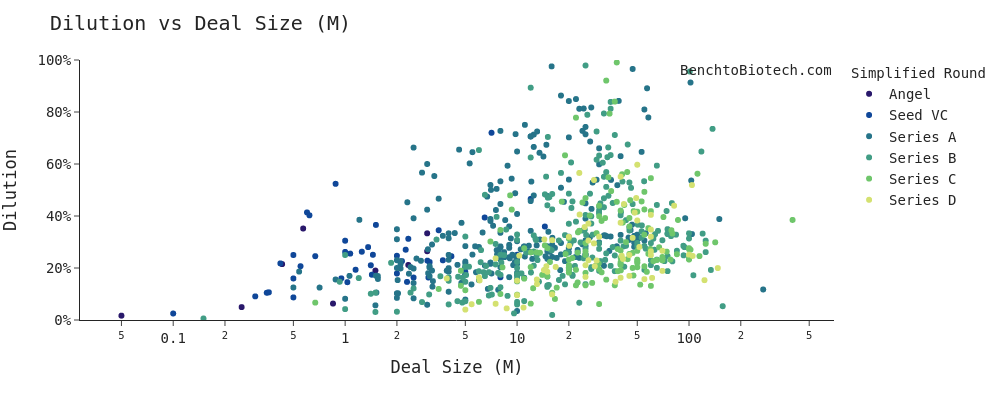

But maybe those companies weren't raising as much money? Indeed, you see that there is a loose correlation between deal size and dilution, with bigger rounds resulting in more dilution. But this is a pretty imperfect correlation, with many larger Series A and B deals seeing dilution in the 20-45% range.

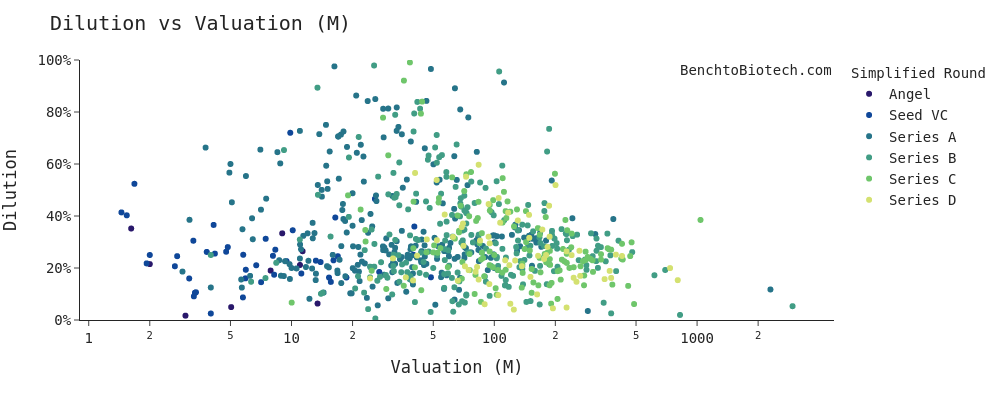

And, conversely, the higher a valuation a company commands, the lower the dilution typically is. This correlates pretty well with standard cap table math.

TL;DR: Outcomes are highly individualized, but it doesn't seem to be an absolute rule that dilution is higher in biotech.

Looking at individual companies

It's hard to know how the per-round dilution on a given company connects to outcomes. It can be worth taking a large dilutive round if you ultimately add a lot of value to the company. Plus, there are a lot of variables based on the novelty and inherent value of a technology, the execution of a team, and the market context.

So it's worth taking a closer look to the full life cycle of a company from inception to exit. Note the same caveats as above, except any errors will be perpetuated through all subsequent rounds. Results may not be representative, and so on.

Still, poke around. It should be illustrative for understanding how dilution and valuations are connected.

Scroll over the dots below to see the per round cap table estimates automagically update. To view the app in full screen mode, go here.